The Market Brief

U.S. futures surged during early trading after Washington and Tehran reached a preliminary agreement to end the Iran war and reopen the crucial Strait of Hormuz.

Macro Viewpoint

Last week, the S&P 500 gained 0.6% as investors digested a strong payrolls report alongside a benign CPI print.

Hedge funds net bought U.S. equities for a fourth straight week at the fastest pace since November 2025, driven by short covering in macro products. Single stocks were modestly net sold, led by weakness in Info Tech.

Info Tech was the worst-performing sector by a wide margin, though trading flows show no signs of panic; the magnitude of selling remained modest relative to the price drawdown.

Prime Intelligence

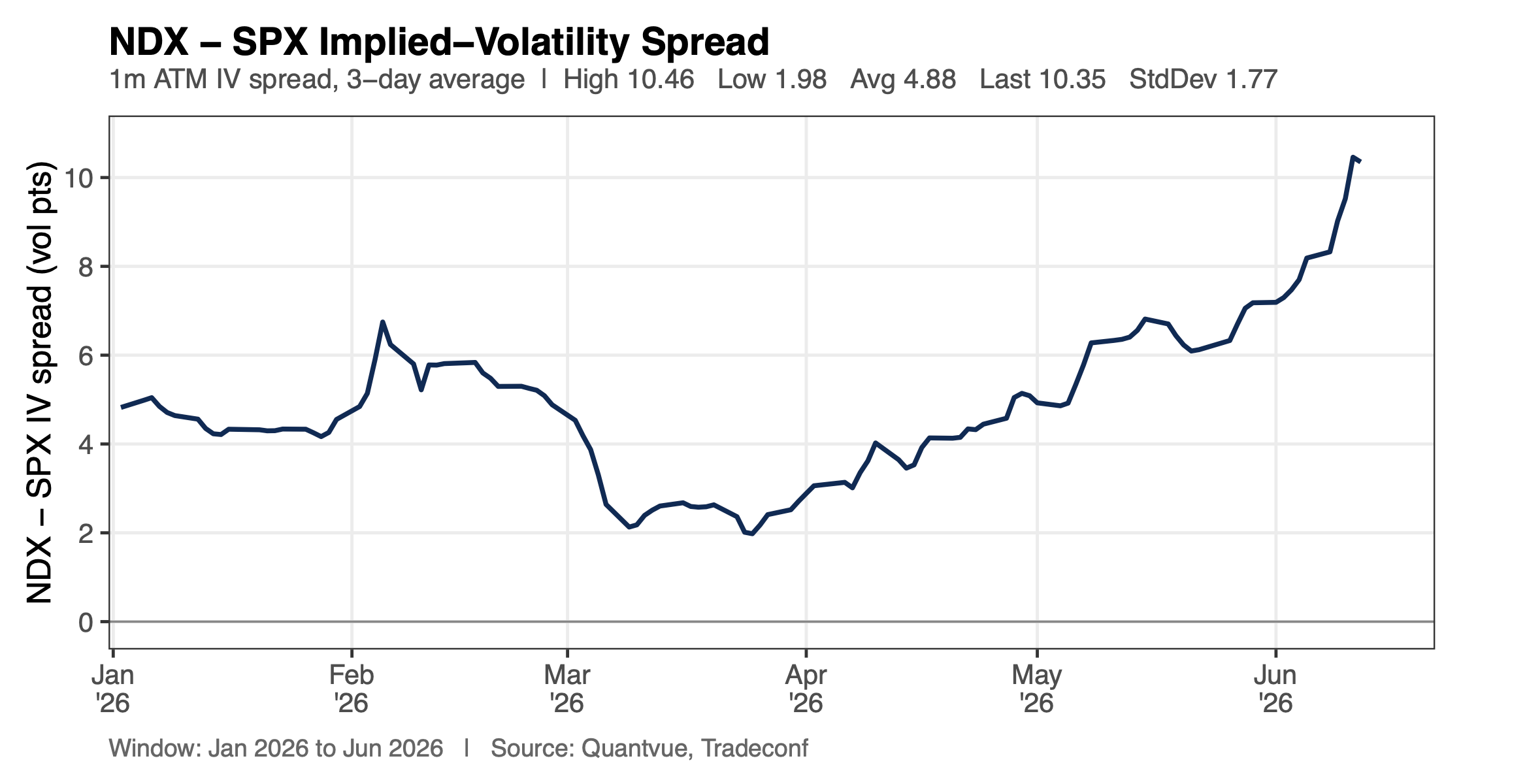

One of the most notable dynamics in options right now is the NDX-SPX implied volatility spread. Implied vol is simply what the market is pricing in for future movement.

That spread currently sits at roughly 10.5 vol points, ranking in the 99th percentile on a 20-year lookback. In short, options markets are pricing far more risk into tech than into the broader market. On Wednesday, NDX posted its largest intraday implied vol range since Liberation Day.

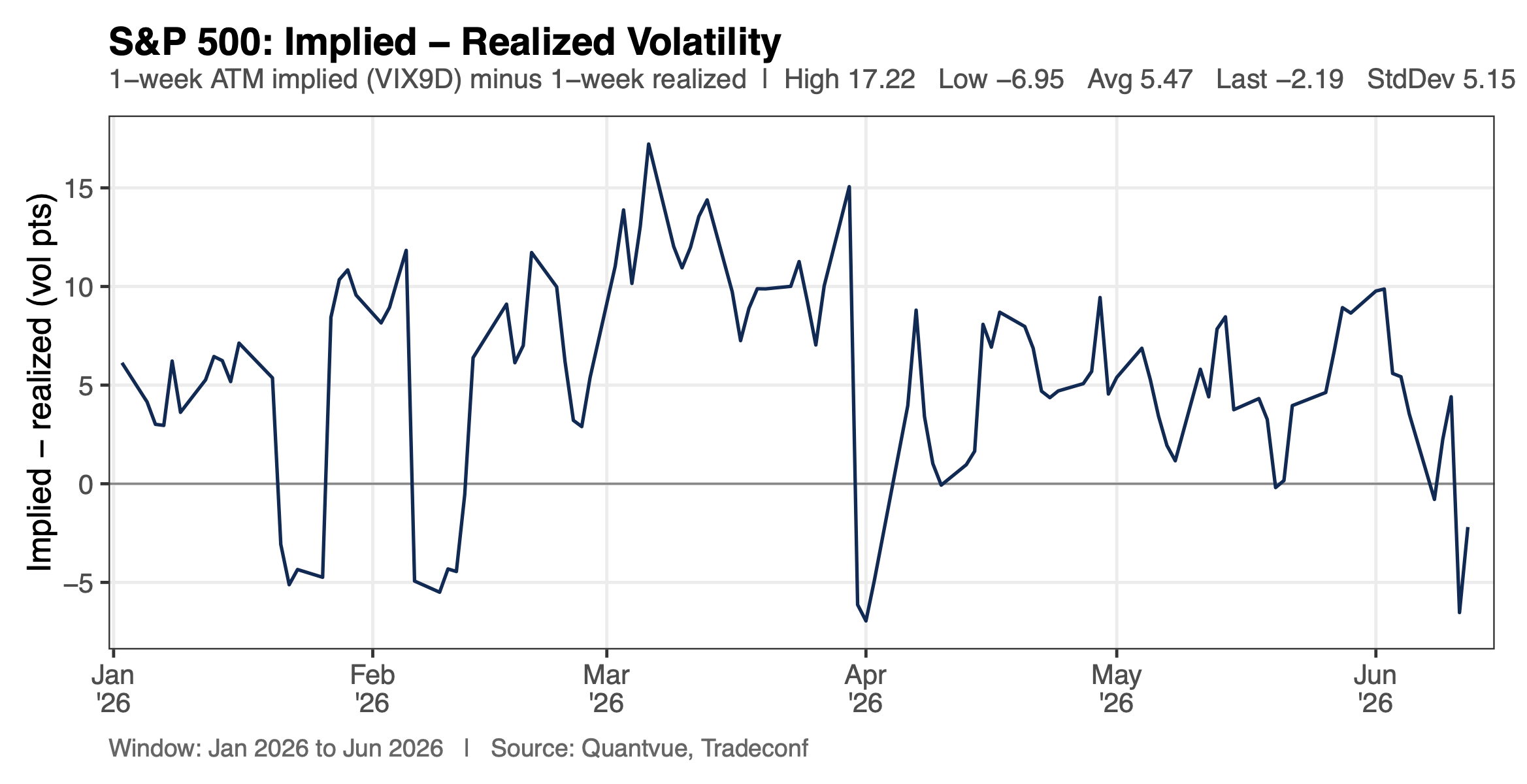

On the SPX side, realized vol has been running above what options priced in, pushing the implied-realized spread to near one-year lows. That environment favors owning options, and we continue to like SPX options to capture catalysts over the next few weeks.

Despite large intraday swings, broader fear is absent. The S&P 1-month normalized put/call skew has flattened for four straight sessions and hovers near one-year lows as institutional clients moved to monetize hedges.

The Market Brief

📰 In today’s brief we track where systematic strategies are positioned across major U.S. equity benchmarks and what price levels could flip the entire trade.

Get access to our full research by becoming a subscriber.

Join hundreds of subscribers already on the inside 👇