Hedging Risk

Hey team. The S&P 500 index edged down 0.2% this week as gains in the energy, technology, and financial sectors were outweighed by declines elsewhere, followed by peak geopolitical tensions.

Let’s see what’s ahead for the markets!

Impact Snapshot

Services PMI - Monday

Consumer Confidence - Tuesday

Q1 GDP - Thursday

Unemployment Claims - Thursday

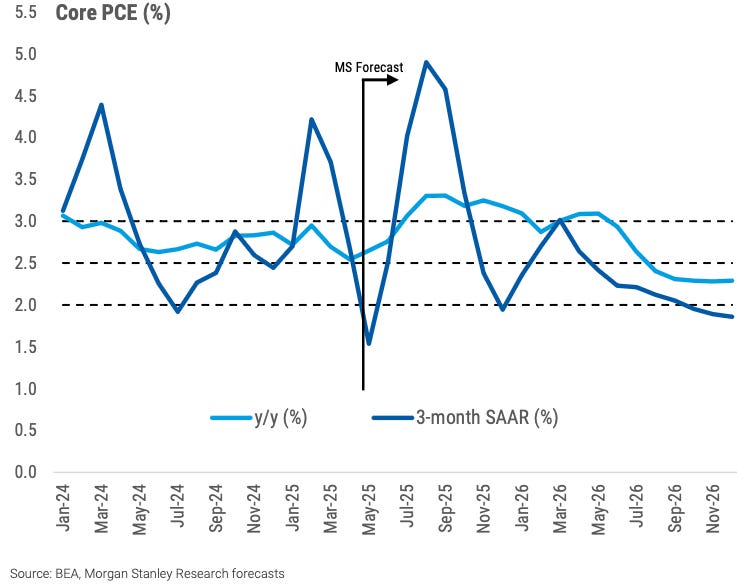

PCE Inflation - Friday

Consumer Sentiment - Friday

Macro Viewpoint

At its June meeting, the Fed kept the target range for the federal funds rate unchanged at 4.25–4.50%, and there was no change in balance sheet policy, as expected.

According to some Wall St. banks, they maintain their view that the uptick in inflation will occur over the summer, before the growth slowdown.

The FOMC continued to see policy as well-positioned to respond to the economic effects from tariffs. During the press conference, Chair Powell emphasized that they are waiting to see how the inflation data will respond to tariffs over the summer, and how the labor market will evolve.

While the reaction function remains the same, emphasizing distance from the target for both objectives and the time it takes to achieve them, the FOMC members’ forecasts showed wider dispersion around economic outcomes.

Wall St. Prime Intelligence

During last Tuesday’s overnight brief, it appears we have called the pullback potential to the exact day and projected clear warnings for our Subscribers. Three straight red days on the S&P followed.

On that brief we shared evidence that we saw institutional money managers hedging downside risk along with our thesis as to why the market was likely faced with a short-term pullback. (Read entire report if you’re a subscriber here)

We’re not here to predict when someone presses a button. We’re here to asses risk and evaluate market conditions based on data we get from trading desks that move “actual size”.

In today’s Prime Intelligence, we share updates on:

Institutional positioning

Implication headwinds

Is the bottom in or more trouble ahead?

What’s next for the markets?

This is a free edition of the Market Brief. To receive our additional in-depth research and data analysis, please consider becoming a paid subscriber.