The Market Brief

Hey team. U.S. Stock futures slipped early Wednesday as investors sought details on a trade policy consensus reached between the U.S. and China.

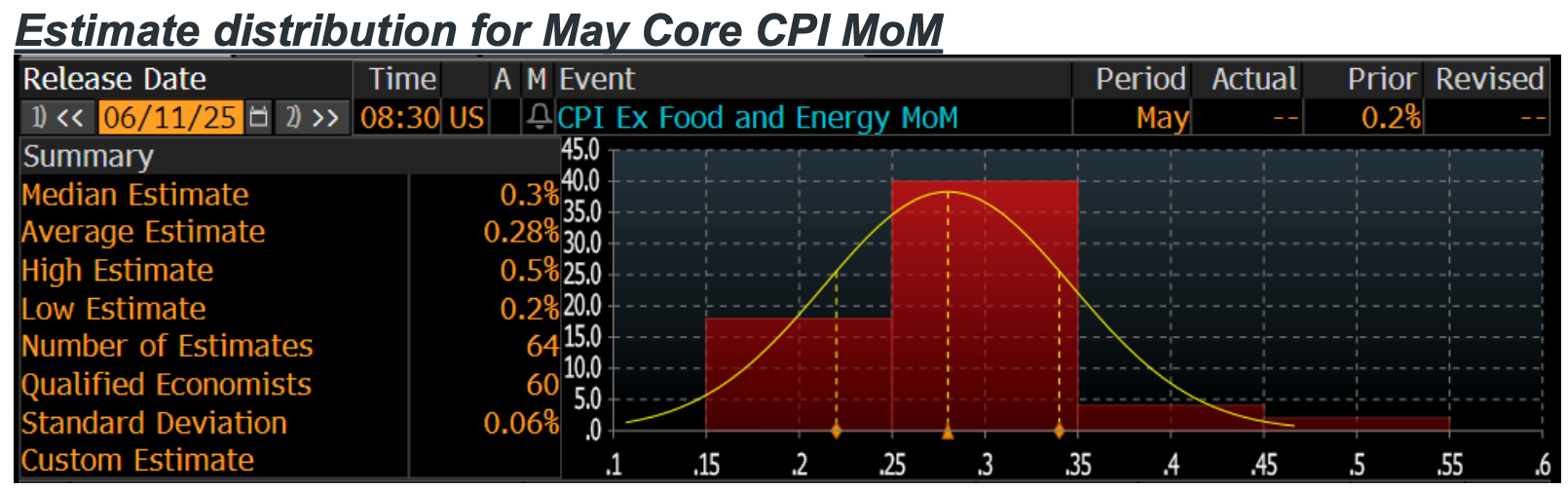

Here is what we’re looking for May’s consumer inflation report today.

Impact Snapshot

🟥 CPI Inflation - 8:30am

🟧 10-y Bond Auction - 1:01pm

Macro Viewpoint

US stock futures slipped after the outcome of pivotal trade negotiations between the Trump administration and China lacked the detail needed to lift markets hovering near all-time highs.

CPI Scenarios For Today

[5.0%] Core MoM prints above 0.40%. SPX loses 2% - 3%. A print of this kind would likely map to higher than expected inflationary impulse from the trade war.

[25.0%] Core MoM prints between 0.35% - 0.40%. SPX loses 1.25% - 1.75%. Bonds would react negatively to this type of print and think any additional cuts would be priced into later in the year given the expectation for a spike in inflation this summer.

[35.0%] Core MoM prints between 0.30% - 0.35%. SPX loses 0.25% to gains 0.75%. The base case outcome range but at the higher end we see a slight sell-off while the lower end of the range continues the rally.

[30.0%] Core MoM prints between 0.25% - 0.30%. SPX gains 1% - 1.5%. Given the recent dovish CPI prints across the G7, we think there is a slightly higher chance that this outcome unfolds, creating a skewed distribution.

[5.0%] Core MoM prints below 0.25%. SPX gains 2% - 2.5%. Look for the bond market to add back at least 2x 25bp rate cuts and for Equities to react positively to the bull steepening that likely ensues.

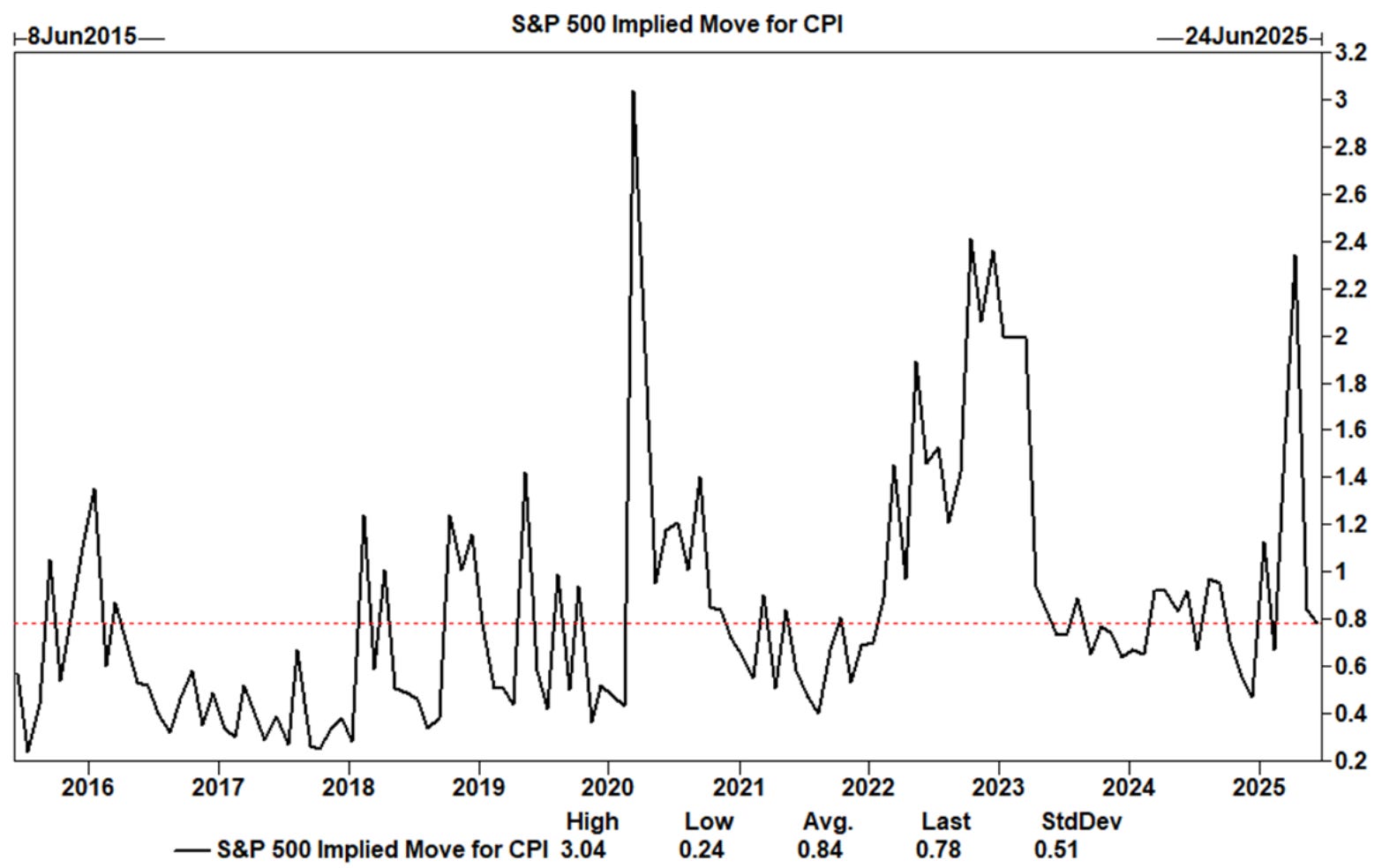

SPX implied move thru today’s close = ~0.78%

We think a dovish print is more likely than a hawkish print given the recent inflation prints in EU/UK; however, positioning suggests that a hawkish print will be punished more than a dovish print will be rewarded.

This is a free edition of the Market Brief. To receive our additional in-depth research and institutional-grade commentary, consider 👉 becoming a paid subscriber.