The Market Brief

U.S. futures are trading lower Friday morning, as geopolitical tensions and renewed AI chip export restrictions continue to weigh on sentiment.

Impact Snapshot

🟥 U.S. Jobs report - 8:30am

🟥 U.S. Retail Sales - 8:30am

Prime Intelligence - NFP

After a week of sharp swings in which investors repeatedly recalibrated their outlook on the duration and impact of the US-Israeli war against Iran.

Non-Farm Payrolls are due today. The distribution of SPX outcomes is skewed to the downside, reflecting elevated uncertainty from the US/Iran conflict.

Importantly, this geopolitical stress has not materially fed through into NFP expectations, with the print likely subdued given softening retail sales forecasts. In this context, a stronger read would be the more constructive outcome, as energy-driven inflation expectations are already moving higher.

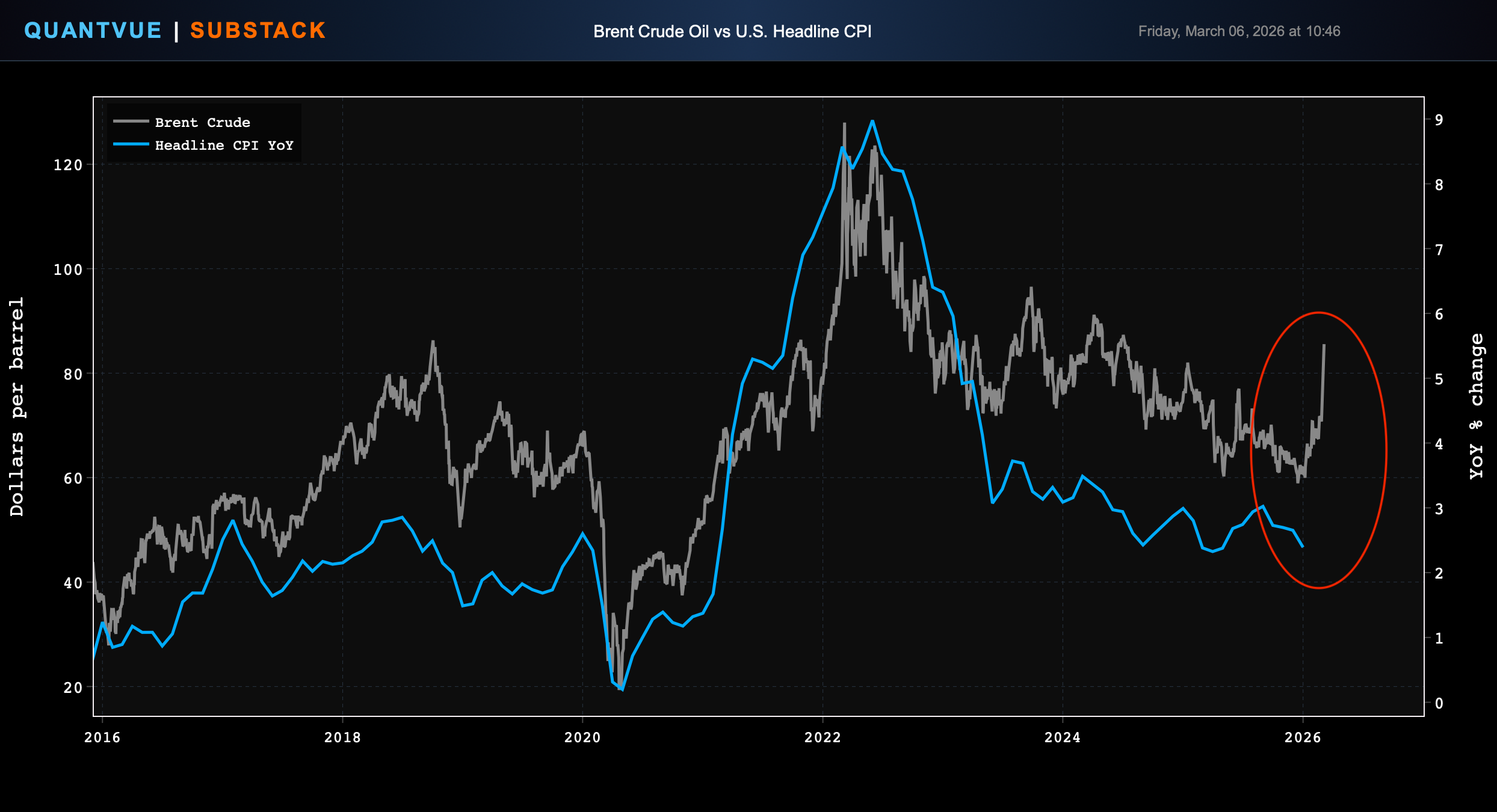

Oil has moved sharply higher and the chart below shows why this can be a problem for inflation. Historically, energy prices are a leading input to headline inflation, and this gap tends to close.

A weak print would reinforce rate cut expectations, but the more pressing risk is stagflation. Slowing growth alongside energy-driven cost-push inflation is a difficult regime for both equities and fixed income.

The Market Brief

CTAs are systematic, trend-following strategies whose positioning can have an outsized impact on market direction and volatility.

In today’s brief, we break down current CTA positioning across key equity indices, what a continued unwind could mean for markets, and where the critical signal-flip levels sit.

Subscribe to read the full analysis.👇