The Market Brief

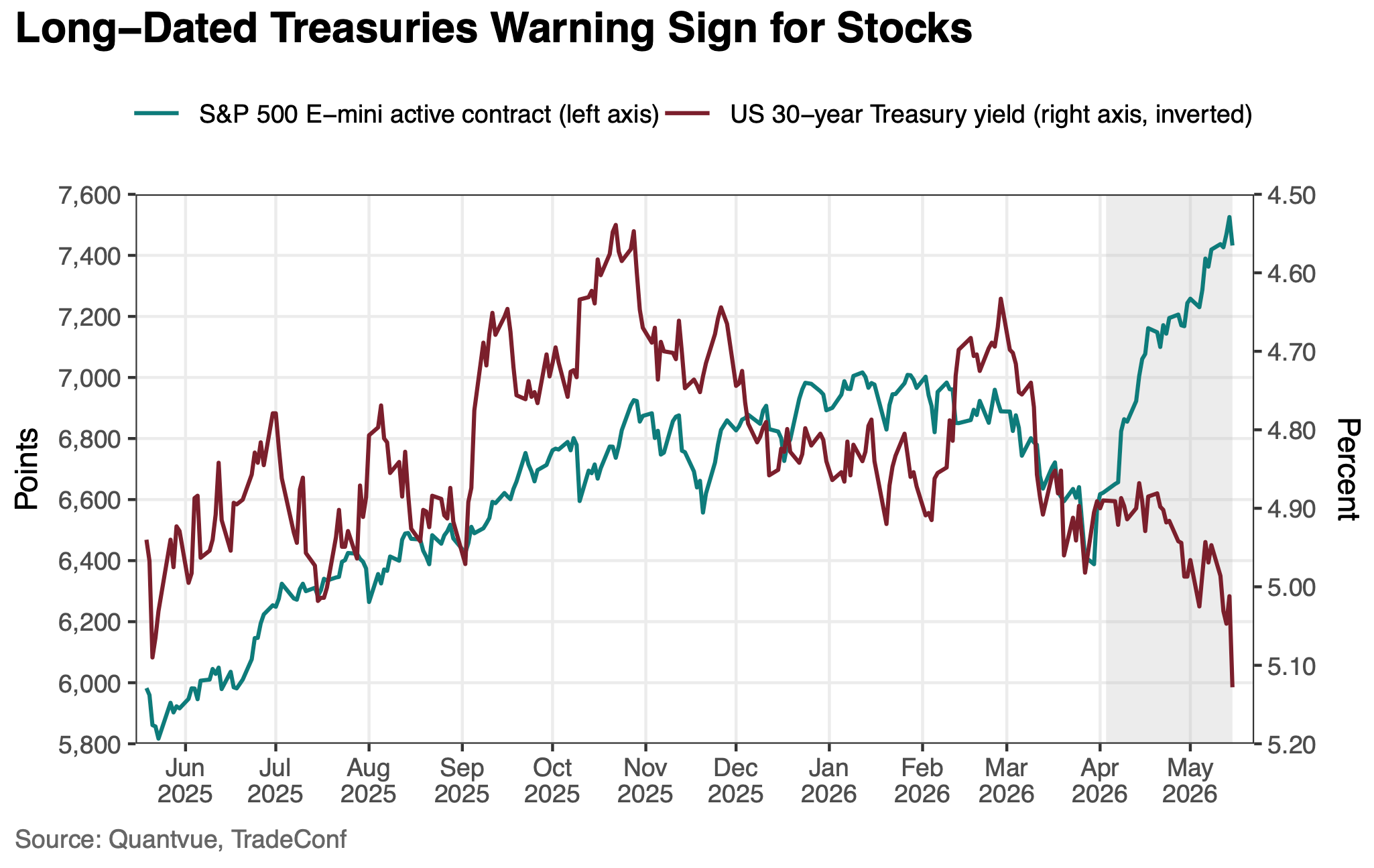

US equity futures slipped Monday as stalled US-Iran negotiations continued to push oil prices higher, while bonds remained under pressure following last week's global selloff.

Macro Viewpoint

The Middle East standoff, now entering its third month, shows no signs of resolution, weighing on the AI-driven rally that had pushed global stocks to record highs.

Bond yields have climbed to multi-decade levels as markets price in higher rates and increased government borrowing to offset rising energy costs.

Corporate earnings remain a key test. NVDA 0.00%↑ , the world’s most valuable company, reports Wednesday as a broadly strong earnings season draws to a close.

Prime Intelligence

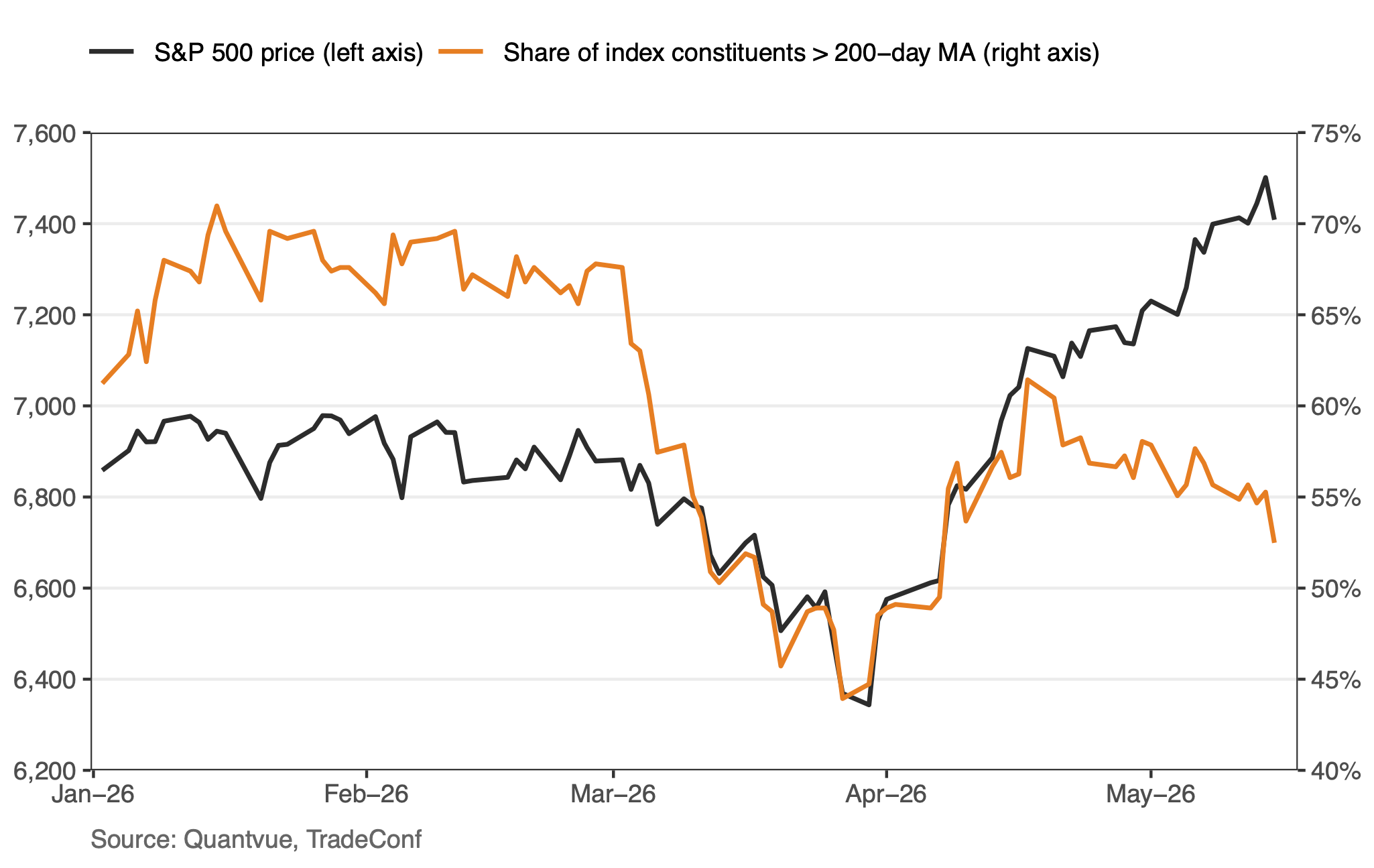

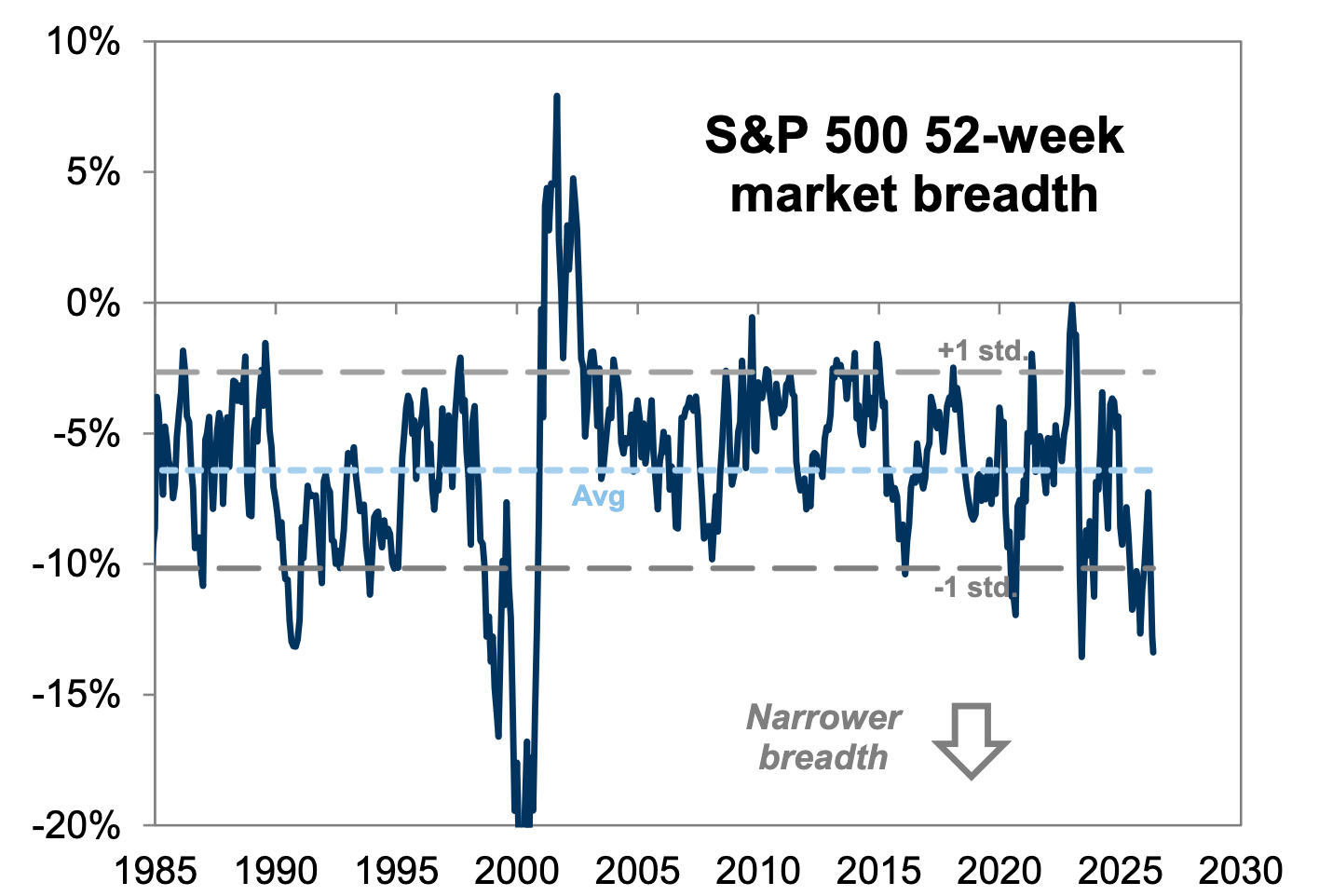

The S&P 500 has returned 10% YTD, with technology accounting for 85% of the index return and the S&P 500 excluding technology returning just 3%.

During the past month, as the S&P 500 has climbed to register 14 new record highs, the share of index constituents trading above their respective 200-day averages has declined.

However, today’s narrow breadth is not necessarily a bearish directional indicator for the equity market. Comparably narrow breadth in May 2023 preceded a period of S&P 500 volatility during the following few months but not the end of the bull market, and breadth today is far less narrow than the market in 1999-2000

The Market Brief

In today’s brief we cover three market indicators painting a nuanced picture of where we stand heading into the week.

The setup is more complex than the price action suggests.

Find out why.👇

Join hundreds of subscribers already on the inside 👇

This is a free edition of the Market Brief. To receive our additional in-depth research and data analysis, please consider becoming a paid subscriber.