The Market Brief

U.S. stock index futures near flat early Thursday as investors remained on the sidelines ahead of the June employment report.

Impact Snapshot

🟥 Non-Farm Payrolls - 8:30am

🟥 Unemployment Rate - 8:30am

Macro Viewpoint

Markets closed lower in choppy trading Wednesday after Federal Reserve Chair Kevin Warsh said inflation risks had eased but vowed to hold firmly to the Fed’s 2% target, warning he would “disappoint” anyone expecting looser policy.

Recent data pointing to a stable labor market could give the Fed more room to hike rates without risking major fallout for employment.

Adding to the uncertainty, the U.S. and Iran wrapped up a round of indirect talks Wednesday with no sign of progress toward a lasting peace.

Prime Intelligence

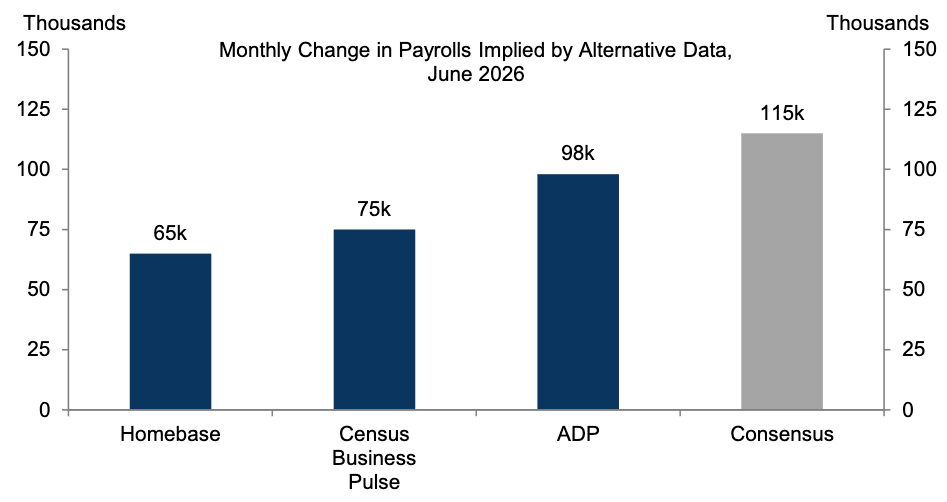

NFP is today: the June jobs report drops at 8:30am ET, released a day early this week (Thursday instead of Friday) due to the July 4th holiday falling on Saturday. Consensus sits at 115k, down from May’s 172k print. Alternative data is running below that bar, with Homebase, Census Business Pulse, and ADP all tracking softer at 65k, 75k, and 98k respectively, pointing to downside risk into the print.

If the alternative data proves closer to the mark than consensus, the print likely lands in the lower half of JPM’s scenario range below.

JPM's NFP scenarios for today's print:

NFP prints above 160k. SPX loses 50bp to gains 1.5%

NFP prints between 130k – 160k. SPX gains 75bp – 1.25%

NFP prints between 100k – 130k. SPX gains 50bp – 1%

NFP prints between 70k – 100k. SPX loses 50bp – 1.25%

NFP prints below 70k. SPX loses 1.25% – 2%

The Market Brief

📰 In todays brief we unpack the positioning shift behind last week’s flows, from institutional selling to hedge funds extending their buying and retail stepping back in for the first time in weeks. We also break down a growing divide in market structure, where record trading volumes are colliding with the thinnest futures liquidity of the year.

Join hundreds of subscribers already on the inside 👇