The Market Brief

Futures were muted Monday as US-Iran peace talks stalled, with investors awaiting a heavy earnings slate and the Federal Reserve's rate decision later this week.

Macro Viewpoint

US stocks held near record highs to open a week packed with megacap tech earnings and central bank decisions, as Hormuz remains shut following a breakdown in US-Iran talks.

Earnings have been a tailwind. Of the 139 S&P 500 companies that have reported, 81.3% have beaten expectations, above the prior four-quarter average of 78.1%.

The S&P 500 has fully recovered its conflict-driven losses, led by chipmakers and an earnings season that has broadly surprised to the upside.

Prime Intelligence

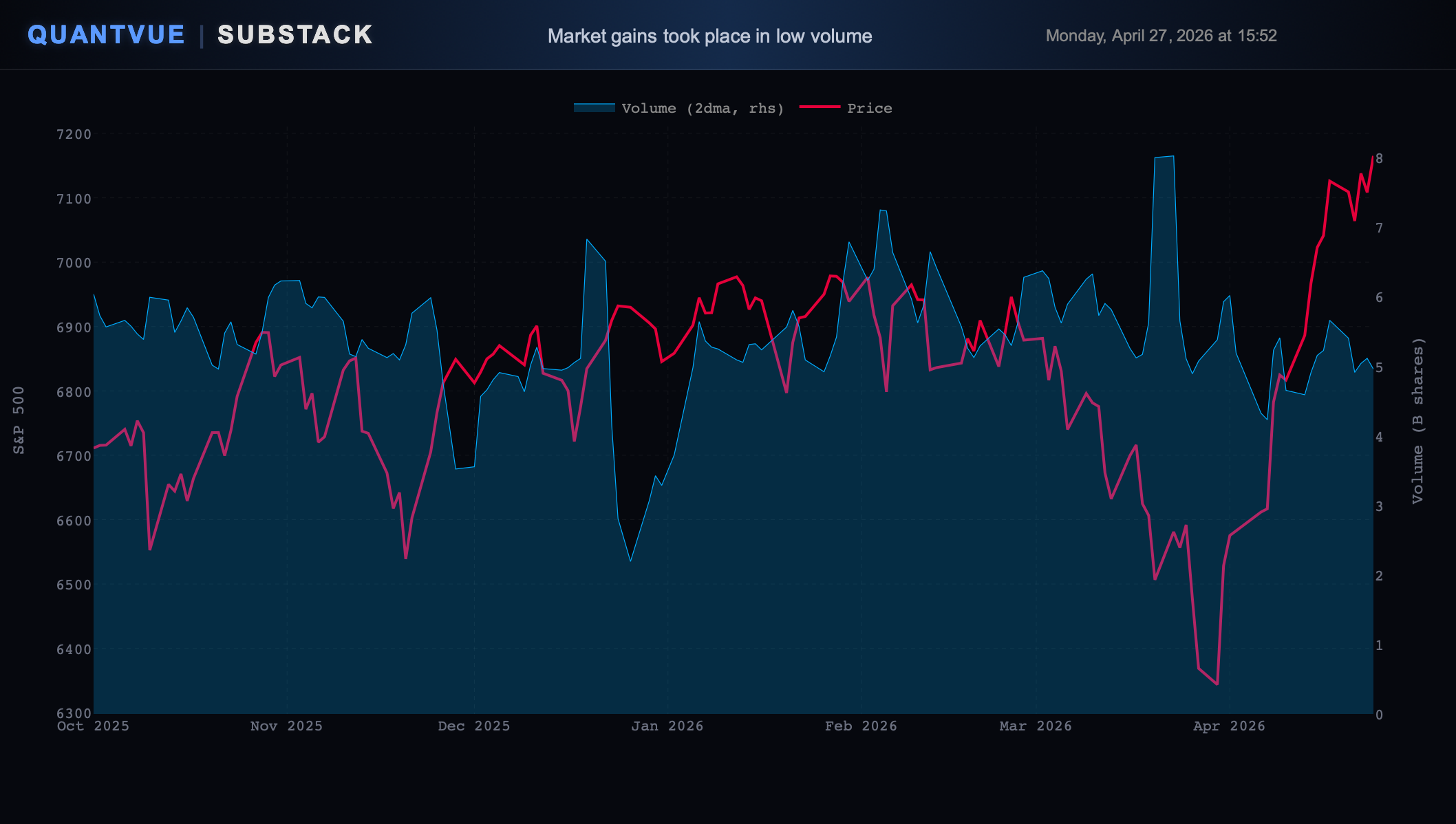

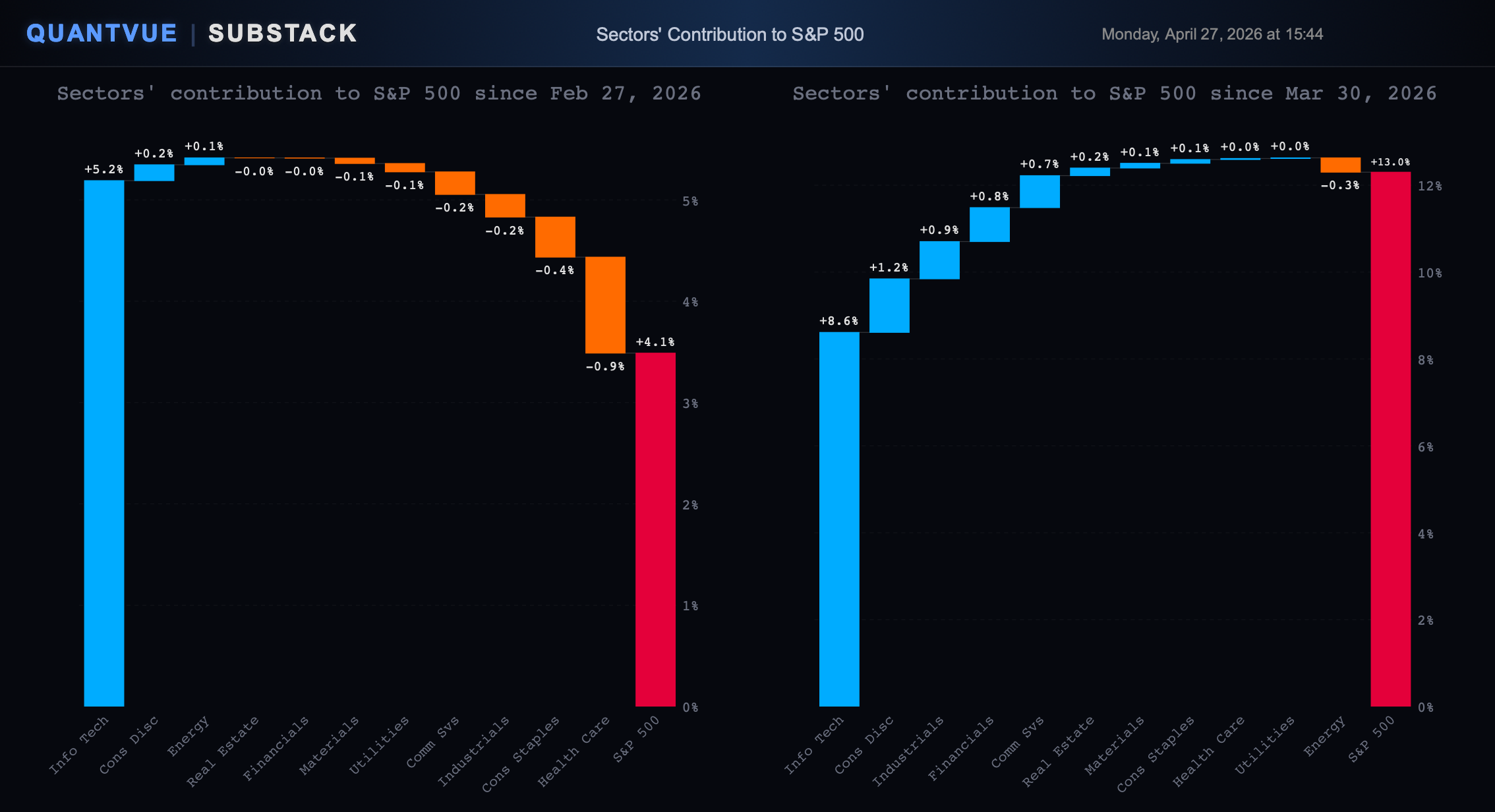

The new highs came on low volume. The short squeeze was triggered by ceasefire hopes between the US and Iran, lower oil prices, and macro fears once again being defeated by micro: earnings expectations met. But few participated in the move off the March bottom.

The breadth tells the story. Since the March 30 low, Tech (Info Tech and Comm Services) has accounted for the lion’s share of index gains, with Consumer Discretionary, Industrials, and Financials filling in the rest. Since the onset of active conflict, Tech alone has driven the entire index return. Every other sector, in aggregate, has been a net drag.

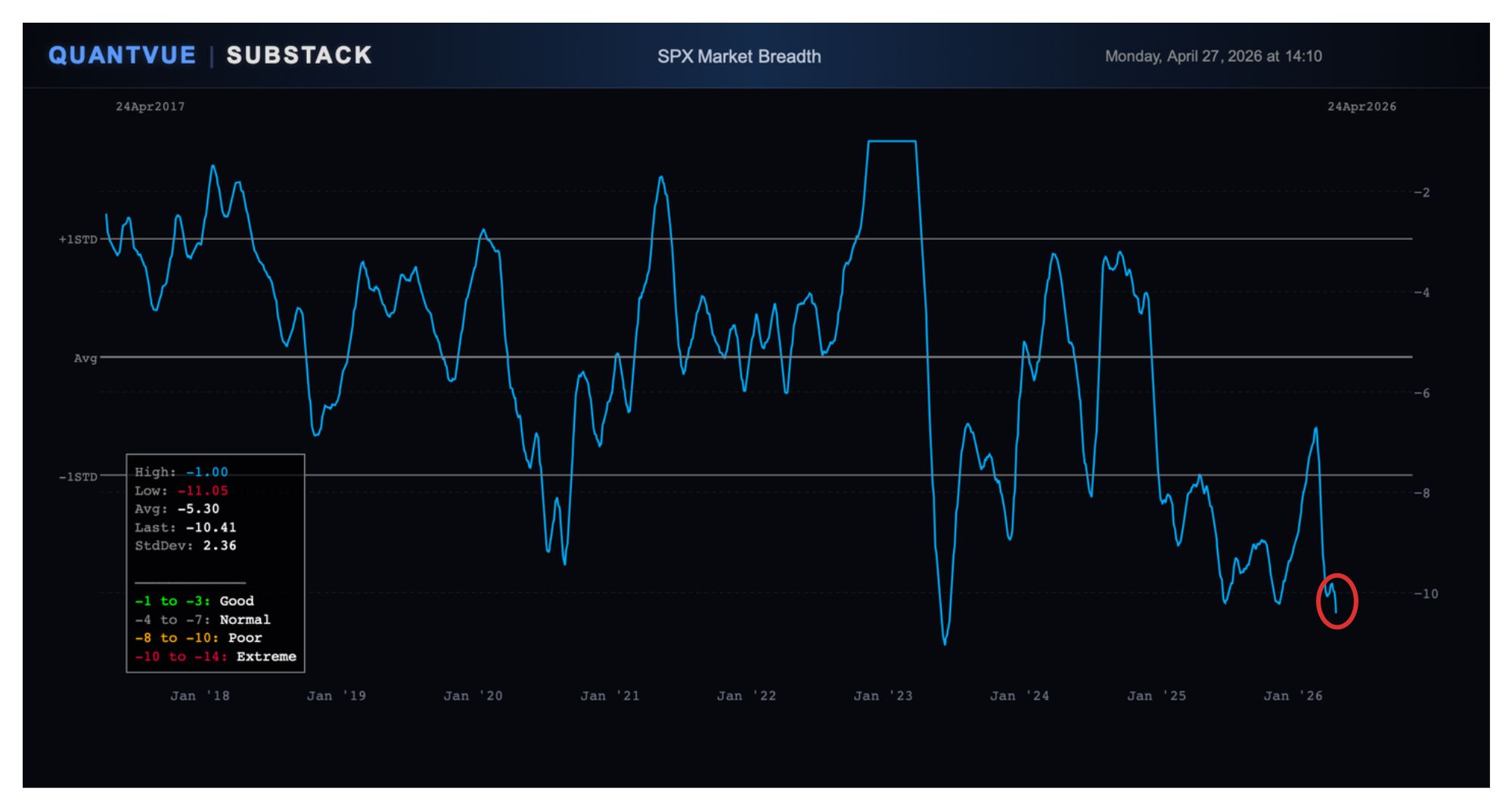

Beneath the surface, dispersion is widening. Friday’s all-time high was driven by just 35% of the index. The headline number flatters what is, for now, a narrow and fragile advance.

Institutional investors who sat out the rebound may feel pressure to chase. Whether that chase broadens participation or simply extends the concentration is the question that matters most going into month-end.

The Market Brief

📰 In today’s brief we map every SPX episode since 2009 where the index reclaimed a prior peak after a 10%+ drawdown, and what history says happens next.

We also flag why the month-end close may not be as clean as the headline suggests.

Get daily institutional insights by subscribing 👇