The Market Brief

S&P 500 and Nasdaq futures recovered Wednesday, clawing back the prior session's losses ahead of key economic data.

Impact Snapshot

🟥 PPI Inflation - 8:30am

Macro Viewpoint

The S&P 500 and Nasdaq eased from recent highs after April CPI posted its sharpest increase in three years, reviving concerns that the disinflationary trend has stalled.

Rate cut expectations have largely been priced out for the year. The probability of at least a 25-basis-point hike by December has climbed above 28%, up from below 22% earlier in the week, shifting the policy narrative meaningfully in a short window.

Compounding the outlook, investors remain cautious that a prolonged conflict keeps energy prices elevated, adding a second channel of inflationary pressure and further complicating the Fed’s path forward.

Prime Intelligence

Risk appetite has rebounded sharply. Positioning is higher, sentiment has turned, and the vol market shows investors actively chasing upside. None of this is surprising; it is precisely what we flagged a month ago. The pain trade has been to the upside, and the flow data now confirms it.

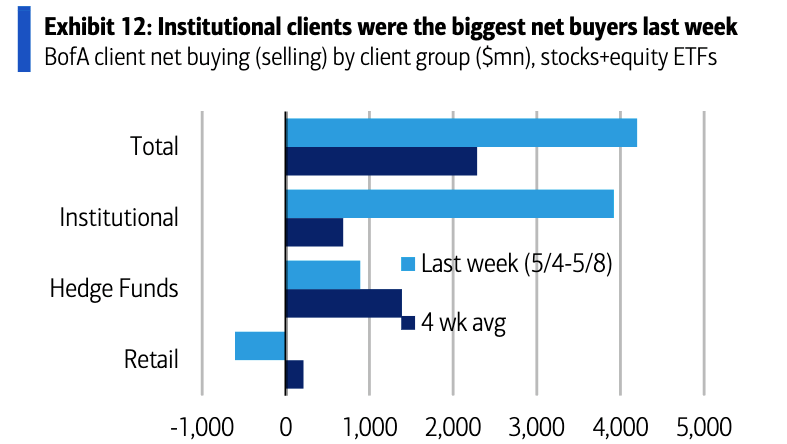

BofA client flows for the week of 5/4-5/8 show institutional investors as the dominant net buyers, running well above their four-week average.

The rally is narrow and concentrated in Tech, which also attracted the largest inflows over the period. This is not a broad-based rotation; it is a targeted chase into the names that caused the most pain on the way down.

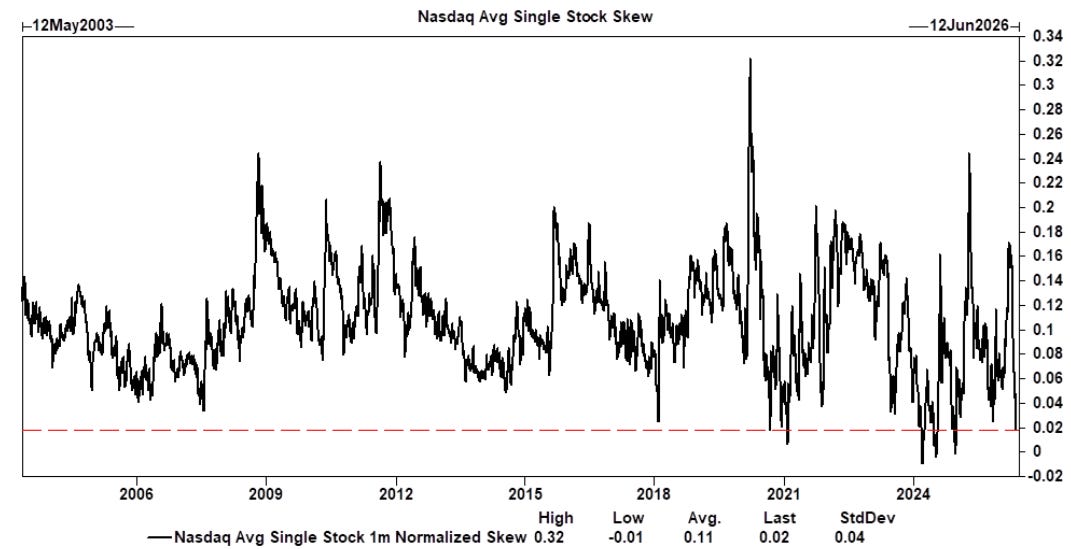

That chase is visible in the options market as well. The average put-call skew across single stocks in the Nasdaq is near its flattest level on record, reflecting investors bidding up calls relative to puts. Demand for upside exposure has overtaken demand for protection.

The Market Brief

In today’s brief we cover the current gamma regime and what it means for realized volatility going forward, the historic breakdown in NDX spot-vol correlation, and what the lack of hedge demand is telling us about the true nature of yesterday’s risk-off move.

Join hundreds of subscribers already on the inside 👇