The Market Brief

US stock futures edged higher early Monday, even as escalating Middle East tensions pushed oil prices and bond yields higher.

Macro Viewpoint

While US stocks found their footing, Friday’s rout left its mark elsewhere. Global markets fell sharply on Monday, with broad-based losses across rate-sensitive sectors.

Investors are starting the week navigating a difficult backdrop: stretched AI valuations, ongoing geopolitical tensions from the Iran conflict, and inflation pressures that are keeping rate hikes firmly on the table.

While the weakness in tech looks more like a correction than the start of a bear market, investors are heading into two weeks packed with event risk.

Prime Intelligence

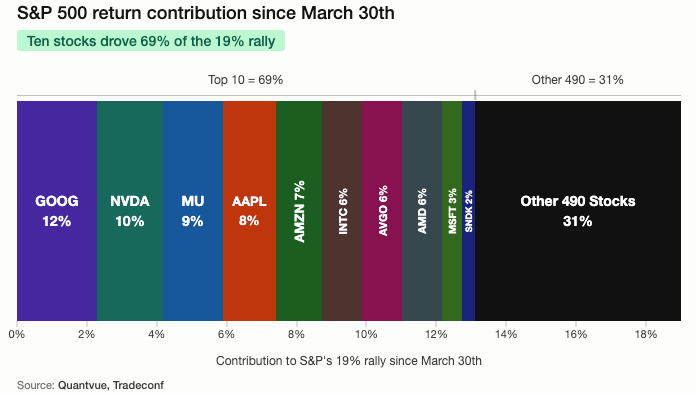

As noted over the past few weeks, the rebound from the March 30th lows has been built on very narrow leadership, and that concentration carries consequences. The S&P 500 has rallied 19% since then, but just 10 stocks have driven 69% of that move.

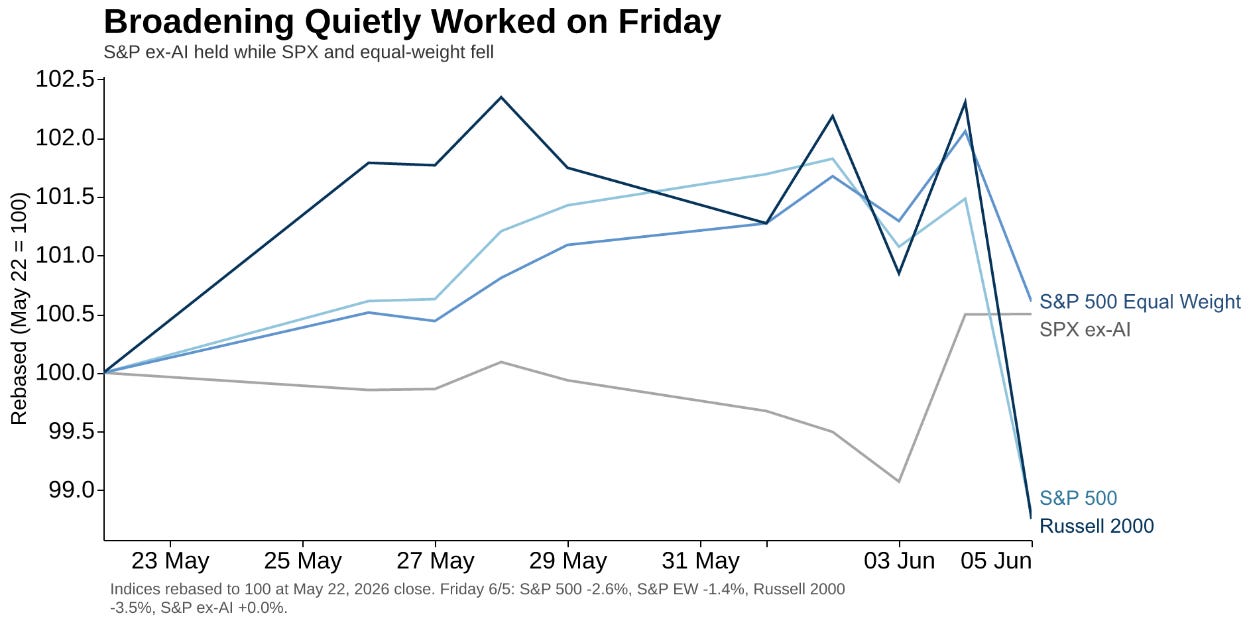

What we flagged in prior briefs was that any genuine broadening of the rally would require those same leaders to sell off first, freeing capital to rotate into laggard stocks and sectors before the market rebuilds its footing. Friday showed exactly that dynamic playing out beneath the surface.

While the SPX fell 2.6%, equal-weight declined 1.4%, and the Russell 2000 dropped 3.5%, the S&P 500 ex-AI index finished the session flat to positive. Small Caps ex-AI also materially outperformed the broader Russell. Friday looked far more like a violent factor unwind than indiscriminate equity selling.

The Market Brief

In today’s brief we break down what actually drove Friday’s selloff, separating the mechanical from the fundamental. We look at whether the options market is telling us something the tape isn’t.

Join hundreds of subscribers already on the inside 👇