Uncertainty Overload

The fast-moving conflict across the Middle East is heightening investor anxiety as markets head into a heavy week of economic data.

Impact Snapshot

ISM Manufacturing PMI - Monday

ADP Non-Farm Payrolls - Wednesday

ISM Services PMI - Wednesday

Unemployment Claims - Thursday

Unemployment Rate - Friday

Macro Viewpoint

The S&P 500 finished February with a modest loss on the month as investors have been positioning around elevated volatility in Tech, Financials, and anything tied to the AI disruption trade.

US equities were net sold for a 2nd straight week, as HFs unloaded Single Stocks at the fastest pace since Liberation Day partially offset by buying in Macro Products. 9 of 11 sectors were net sold led by Financials/Industrials/TMT.

Macro traders are watching energy markets and the possibility of prolonged turmoil in the Middle East, which could lead to higher oil prices and a shift into safety.

Setting aside the geopolitical risk, the market was already positioned for a move lower. The options market had been telegraphing this well in advance, with positioning and implied volatility structure hinting at the direction of travel before the news broke.

Prime Intelligence

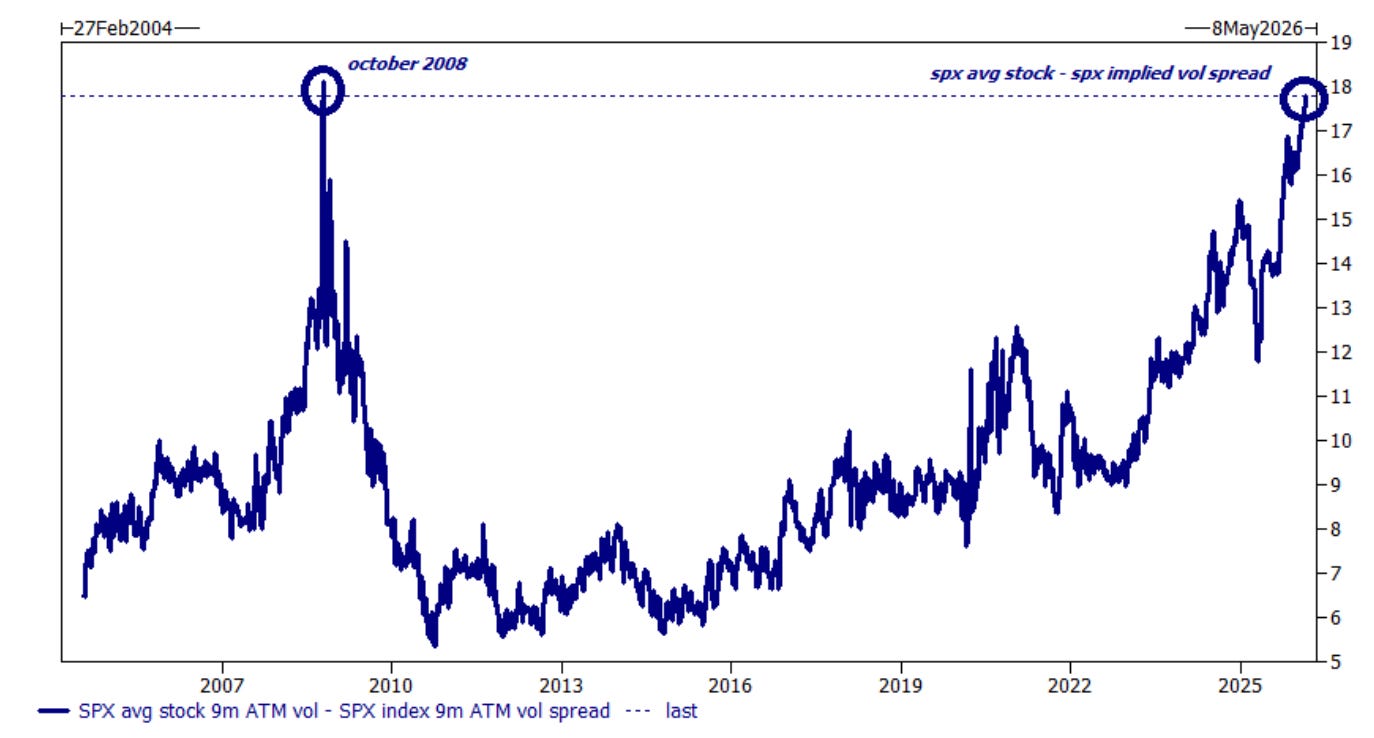

Individual stocks have decoupled from the broader market at a magnitude not seen in decades, making realized dispersion the defining theme of 2026.

For traders hoping equity trading patterns will just “go back to normal” and stocks will once again move in lockstep with the index, the volatility market offers an uncomfortable signal.

Looking out over the remaining ~210 trading sessions through year-end, the implied volatility spread between the average single stock and the index sits at roughly 18 vol points. To put that in context, this is the widest spread observed since October 2008, when the VIX was trading near 80 at the height of the financial crisis.

What does this mean in practice? High dispersion environments historically reward active management. Stock pickers, long/short equity strategies, and alpha-focused managers tend to outperform when individual names diverge sharply from the index, as the current environment creates meaningful return differentiation across securities rather than broad, correlated moves.

The Market Brief

In today’s brief we discuss why the options market is signaling fear beneath the surface, how systematic strategies are positioning heading into next week, and why negative gamma has the potential to amplify volatility.

Subscribe now to read the full brief👇