Almost There

Hey team. The Standard & Poor's 500 index rose 1.5% this week as May payrolls came in above expectations.

Let’s recap last week and see what’s ahead!

Impact Snapshot

CPI Inflation - Wednesday

10-y Bond Auction - Wednesday

PPI Inflation - Thursday

Unemployment Claims - Thursday

Consumer Sentiment - Friday

Inflation Expectations - Friday

Macro Viewpoint

The S&P 500 gained +1.5% on the week (now only 144 handles from ATH seen on 2/19) and index volatility continued to compress as investors digested a mix of hard (May NFP report) and soft (ISM Manufacturing and Services surveys) data that point to a reasonably resilient US economy.

Despite the “noise” out of DC, markets continue to repair as the worst of the feared economic fallout fails to materialise.

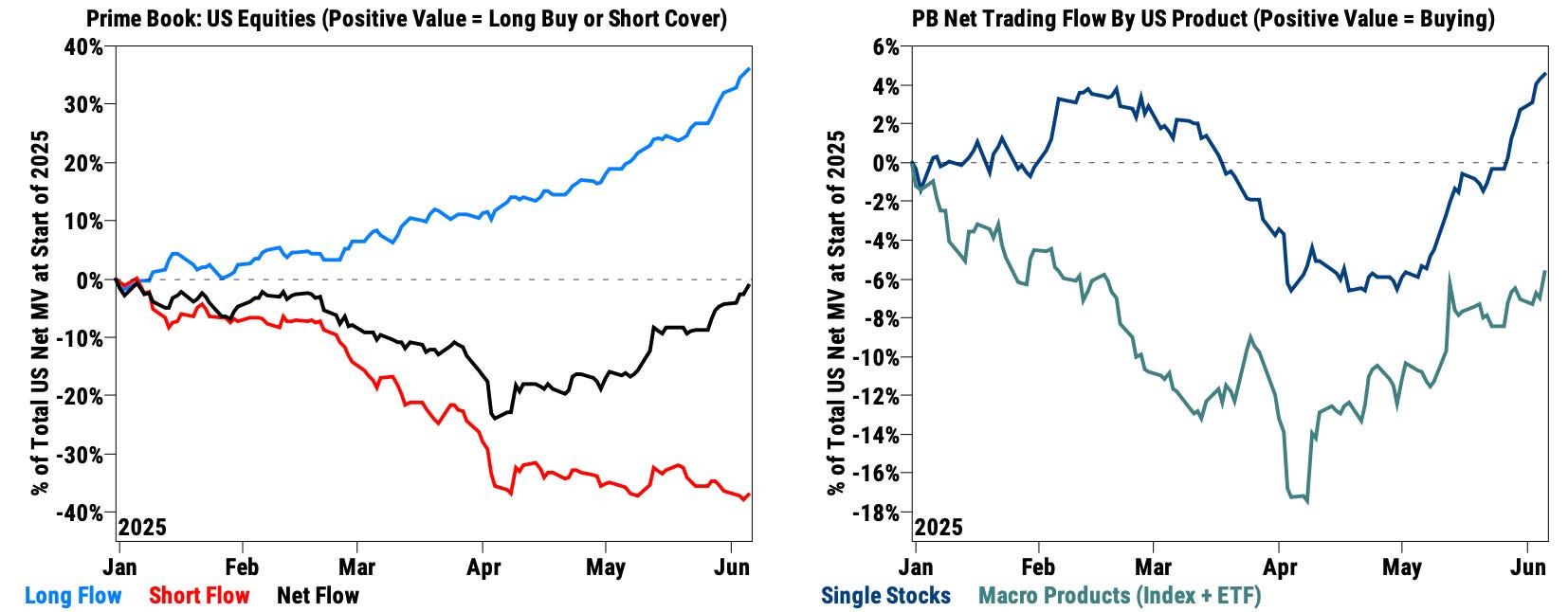

Global equities were net bought for a 5th straight week (+0.8 SDs 1-year) while gross trading activity saw the largest increase in 2 months, driven by long buys outpacing short sales (1.7 to 1). Buying in North America outpaced selling in every other major region

There is a huge & unprecedented level of cash on the sidelines. $7trln of money market fund assets is still a tricky number to contextualise or factor into the macro framework.

Wall Street Prime Intel

We first made the case back on Apr 6 that the market fell into support at 4800, and we anticipated institutional clients to add risk.

Throughout this entire rally, we’ve been reiterating our bias, sharing actionable evidence and models to support our thesis that the risk was skewed to the upside, which you’re free to check any day of the week through this Brief’s archives.

Fast forward 2 months later, and we’re almost close to ATHs.

Read our up-to-date research on where we think this market is going.👇

This is a free edition of the Market Brief. To receive our additional in-depth research and data analysis, please consider becoming a paid subscriber.