The Market Brief

U.S. futures edge higher, with strong earnings easing concerns over a potential tariff-related slowdown and lending support to elevated stock valuations.

Impact Snapshot

🟥 PCE Inflation - 8:30am

🟥 Employment Cost - 8:30am

🟥 Unemployment Claims - 8:30am

🟥 Key Earnings(after close): AMZN 0.00%↑ AAPL 0.00%↑

Macro Viewpoint

As we expected, the Fed held rates in the 4.25%-4.50% range (for the 5th consecutive time). The Statement was broadly in line with our key takeaways from yesterday’s brief, pointing to a growth slowdown acknowledgment.

During the Presser, Chair Powell’s prepared remarks pointed to underlying aspects of inflation shifting between Services prices (easing) and Goods (rising) due to ‘Govt policies’ (Tariffs), but longer-term expectations still consistent with the 2% target, with Policy characterised as ‘modestly restrictive’.

This is an economy that grew above 1% with signs of acceleration. Unfortunately, inflation is also accelerating higher.

At this time, there is not a compelling reason to cut unless the labor market is materially weaker than the data suggests. This is a positive for stocks, and it has reflected on the follow-up.

📰 Wall St. Prime Intelligence

Unlike the significant amount of individuals that will completely cloud your vision on how markets operate on the underlying, we continue to provide statistical evidence and data that supported a market higher and shared with our paid Subscribers often weeks or months before the fact.

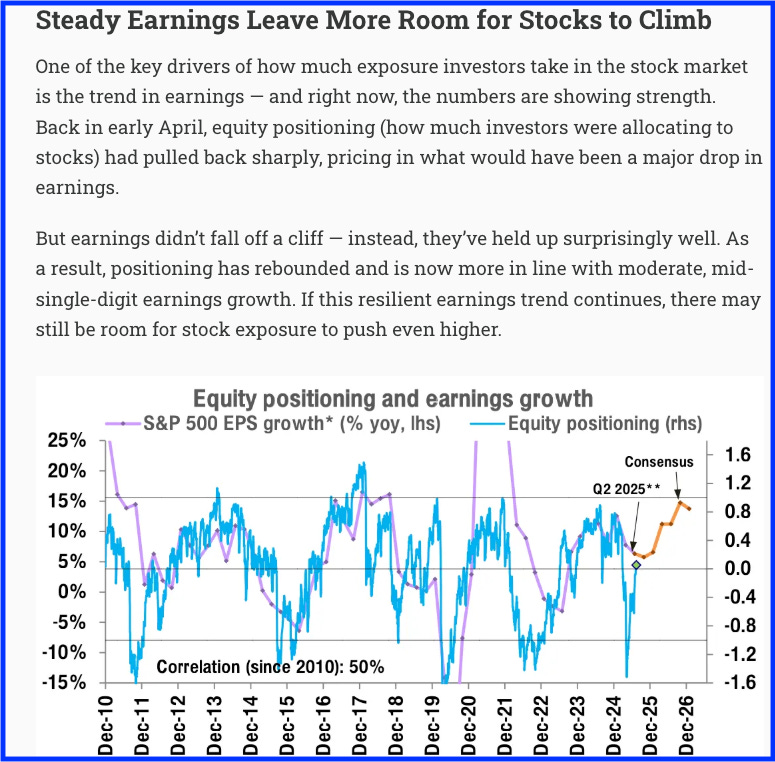

One of the component of our research, which we’ve reiterated 11 days ago, was a forecasting of steady earnings continuing to perform, which would increase the equity exposure.

If you want access to daily institutional-grade research based on actual data and quantitative modeling, consider becoming a paid subscriber.👇